Okay, let's cut right to the chase. The biggest, most fundamental difference between a sole trader and a company in New Zealand boils down to this one simple idea: as a sole trader, you are the business. There’s no legal wall between your work life and your personal life. None at all. A company, on the other hand, is its own separate legal 'person'. This creates a protective barrier for your house and car but, you guessed it, demands a bit more paperwork.

So, you’re about to kick off a new business venture here in New Zealand. That's awesome. But you’ve probably already hit your first major fork in the road: should you set up as a sole trader or register a proper company? It feels like a massive decision because, honestly, it is.

This one choice has a ripple effect on pretty much everything—from the tax you'll pay and the personal risk you'll carry, to the sheer amount of admin waiting on your desk. It can feel a bit much, can't it? Let's break it down in simple terms.

Think of the sole trader path as the "you are the business" route. It's incredibly quick and straightforward. It's the lean-and-mean way to get off the ground with minimal fuss. But—and this is a big but—your personal assets are totally in the firing line if things go pear-shaped.

A company, on the other hand, creates a legal shield around your business. This gives you valuable protection, a bit like a suit of armour, but it expects more formal paperwork in return.

Here's a straightforward, no-fluff summary of the fundamental differences between being a sole trader and operating as a company in New Zealand.

| Feature | Sole Trader | Company |

|---|---|---|

| Legal Status | You and the business are one and the same. No separation. | A separate legal entity from its owners (shareholders). |

| Liability | Unlimited personal liability for business debts. Yikes. | Liability is limited to the company's assets. |

| Setup Cost & Complexity | Super low cost, dead simple to start (just need an IRD number). | Higher setup cost and requires formal registration. |

| Taxation | Business income is taxed at your personal income rate. | Profits are taxed at the flat corporate rate (currently 28%). |

| Admin & Compliance | Minimal ongoing paperwork; file an IR3 tax return. | More compliance; annual returns, shareholder records, etc. |

| Public Perception | Often seen as smaller, individual operations. | Can appear more established and credible to clients/lenders. |

It's easy to see why the sole trader structure is so popular. A huge 74% of all enterprises in New Zealand have zero paid employees, which really shows how many Kiwis go this route. For startups just wanting to test an idea or get launched quickly, it’s the default choice because it’s so simple and cheap—all you really need is your personal IRD number. You can get more insight into why this model is so common in our guide to small businesses in New Zealand.

Which path should you take? There’s no single 'correct' answer; it all comes down to what you’re building.

Are you a freelance copywriter just starting out? The beautiful simplicity of being a sole trader is probably a perfect fit. Or are you planning to hire staff, chase investment, or take on some serious financial risk? In that case, the protection a company structure provides is likely essential. As you think through these early stages, it can also be a big help to check out a broader guide on how to start a small business in NZ.

This guide will walk you through the real-world implications of each, helping you decide what's best for your new venture—whether it's a web design agency in Christchurch or a clever app idea brewing in Auckland.

Right, let’s get to the sharp end of the stick. This is arguably the most critical difference between operating as a sole trader and a company. It’s all about what happens if things go wrong.

When you're a sole trader, you and your business are legally the same entity. There’s absolutely no separation. If the business racks up debt, gets sued, or can't pay its suppliers, your personal assets are fair game. We're talking about your house, your car, your personal savings—the lot.

It’s a sobering thought, and it’s a big deal.

This is what’s known as unlimited personal liability, and it’s the single biggest risk of the sole trader structure. Think of it this way: there's no firewall between your business life and your personal life. A fire in one can quickly spread and cause chaos in the other.

Now, let's look at the alternative. A limited liability company is specifically designed to create a protective wall around you. It does exactly what it says on the tin: it limits your liability.

The company is its own separate legal 'person.' It can sign contracts, own property, and take on debt all by itself.

If the business owes money, creditors can go after the company's assets, but they generally can't touch yours. Your family home is safe. This fundamental separation is the cornerstone of the company structure and provides massive peace of mind for many business owners.

Key Takeaway: For a sole trader, business debt is your personal debt. For a company, business debt belongs to the company, shielding your personal assets.

Of course, there’s always a catch, isn't there?

That protective shield isn't completely bulletproof. When you apply for a business loan, sign a lease for an office, or open a trade account, the lender or landlord will often ask for a personal guarantee.

Signing one of these means you are voluntarily putting your personal assets back on the line. You're effectively saying, "If my company can't pay this debt, I promise I will." In that moment, the protective wall you built has a great big door in it, and you've just handed the key to your creditor.

So, while a company offers fantastic protection, it’s not a get-out-of-jail-free card. You still have to be incredibly careful about the documents you sign.

Let's bring this down to earth. How much this all matters depends entirely on what your business does.

The Freelance Developer: You're coding websites from a home office. Your biggest risks are probably a client dispute or a few unpaid software subscriptions. The potential financial fallout is relatively contained. In this case, the simplicity of being a sole trader might well be worth the small risk.

The Growing Digital Studio: Now, imagine you run a small agency. You've leased an office in Christchurch, hired a couple of staff, and taken out a loan for new gear. Your risk profile has just gone through the roof. If the business fails, you're personally on the hook for the rest of the lease, staff entitlements, and that equipment loan. Operating as a company in this scenario is almost a no-brainer.

Choosing your structure isn’t just an administrative task for the IRD. It's about honestly assessing your business's risk level and deciding how much of your personal life you're willing to gamble on its success. Your answer to that question will probably point you in the right direction.

Alright, let's talk money—specifically, how you and your business look in the eyes of the IRD. The way tax works for a sole trader versus a company is worlds apart, and getting your head around this is the key to keeping more of your hard-earned cash.

This is often the point where the "sole trader vs company" decision really crystallises for people. It’s not just about the legal stuff; it’s about how your profits are handled and what you actually get to take home.

As a sole trader, your business income is your personal income. There's no separation. Whatever profit your business makes (after expenses, of course) gets added to any other income you might have, and you're taxed on the whole lot at your personal marginal tax rate.

Initially, this is beautifully simple. You just file one tax return—an IR3—that covers everything.

But here’s the catch: as your profits grow, so does your tax rate. New Zealand has a progressive tax system, which means the more you earn, the higher the percentage of tax you pay on that income. This straightforward structure can become a lot less tax-efficient once your business really starts taking off.

A company is a different beast entirely. It’s treated as its own legal and tax entity. It pays tax at a flat corporate rate, which is currently 28% in New Zealand. This rate is the same whether the company makes $10,000 or $10 million in profit.

You, the owner, aren't directly taxed on that profit. Instead, you get money out of the business in a couple of main ways:

This separation opens up some smart options for tax planning, particularly for businesses hitting higher income brackets.

The Key Difference: A sole trader's profit is taxed at your personal, escalating tax rates. A company's profit is taxed at a flat 28%, and you're only personally taxed on the money you officially take out.

Ah, provisional tax. It's the term that often causes a bit of a cold sweat for new business owners, but it's not as scary as it sounds.

Because you’re not an employee having PAYE deducted from a weekly paycheque, the IRD needs you to pay your income tax in instalments throughout the year. That's all provisional tax is. This applies whether you're a sole trader or a company.

You’ll typically need to start paying provisional tax once your end-of-year tax bill (your "residual income tax") was more than $5,000 in the previous year. Think of it as the IRD’s pay-as-you-go system for business income, designed to stop you from being hit with one massive, unmanageable tax bill.

Whether you're operating as a sole trader or you're the director of your own company, you'll need to pay ACC levies. This is your cover for personal injuries, and it's not optional.

As a self-employed person (a category that includes both structures), ACC will invoice you directly. The amount is based on your liable income and your industry's risk level. For example, a web developer working in a low-risk office will pay much lower levies than a builder on a construction site. It's all handled automatically; you don't need to sign up, but you absolutely need to budget for the bill when it lands.

Goods and Services Tax (GST) is the final piece of the puzzle. The rules for this are the same regardless of your business structure; it's based on your turnover, not your profit.

You must register for GST if your annual turnover is—or is likely to be—more than $60,000 in any 12-month period. If you’re earning less than that, registration is optional.

Being GST-registered means you need to add 15% GST to your prices. The big advantage, however, is that you get to claim back the GST you pay on your business-related purchases. It does add another layer of admin and filing, but for most growing businesses, it’s just part of the game.

Alright, let's have an honest chat. How much paperwork and life admin can you really handle? Your gut reaction to that question is one of the biggest clues in the whole sole trader vs company debate.

When it comes to pure, blissful simplicity, the sole trader structure wins, hands down. It’s the lightweight, no-fuss option for getting things done.

Your compliance duties are wonderfully minimal. For the most part, you just need to keep good records of your income and expenses, then file your personal IR3 tax return with the IRD once a year. That’s pretty much it. No formal registrations, no annual company meetings, no shareholder drama.

Forming a company is like trading your trusty pushbike for a car. It offers more protection and power, but it definitely needs more maintenance. A company introduces a whole new layer of admin you simply don't have to think about as a sole trader.

Suddenly, you’re dealing with two government bodies instead of just one.

It's a genuine step up in complexity, and that brings more potential for things to go wrong if you're not on top of it.

You have to maintain a shareholder register, keep minutes of company decisions, and technically hold an annual meeting—even if it's just you, alone in a room, talking to yourself. It can feel a bit absurd, but it's all part of the formal process.

This bigger administrative load often means you need more support. While you can do it all yourself, this is usually the point where the cost of a good accountant shifts from a 'nice-to-have' to an essential business expense. You're not just paying them to file a tax return; you're paying for the peace of mind that all the boxes have been ticked correctly.

Let's lay out the exact requirements from both the IRD and the Companies Office. Seeing it all side-by-side makes the difference crystal clear.

| Compliance Task | Sole Trader Requirement | Company Requirement |

|---|---|---|

| Initial Setup | None. Just let the IRD know you're self-employed. | Formal registration with the Companies Office. |

| Annual Reporting | File a personal IR3 tax return with the IRD. | File an annual return with the Companies Office AND a company IR4 tax return with the IRD. |

| Record Keeping | Must keep records of all income and expenses. | Must maintain a shareholder register, director details, and formal company records. |

| Bank Account | A separate account is highly recommended but not legally required. | A separate company bank account is mandatory. |

| Employee Admin | Must register as an employer for PAYE if hiring staff. | Must register as an employer for PAYE if hiring staff. May also have Fringe Benefit Tax (FBT) obligations. |

This isn’t meant to scare you off. Thousands of Kiwi businesses manage this perfectly well. But it's about going in with your eyes wide open. Are you ready for this level of formality?

The good news is that modern tools can make this much easier. A lot of this admin can be automated, and for businesses eyeing up growth, investing in things like custom CRM and automation development can turn these chores into a background hum instead of a daily headache.

Ultimately, the choice comes down to a trade-off. A sole trader offers freedom from paperwork at the cost of personal risk. A company offers protection from that risk, but at the cost of more paperwork. It’s a classic business seesaw—you just need to decide which side you’d rather be on.

Maybe you're already cruising along as a sole trader, wondering if it's time to graduate. Or perhaps you're just starting out, trying to map your business journey five years down the track. This isn't just an administrative choice; it’s about making the right call at the right time.

Deciding between a sole trader setup and a company isn't a one-and-done decision. It's fluid. The best structure for your first year of business might become a massive headache in your fifth. The key is recognising the signals for change.

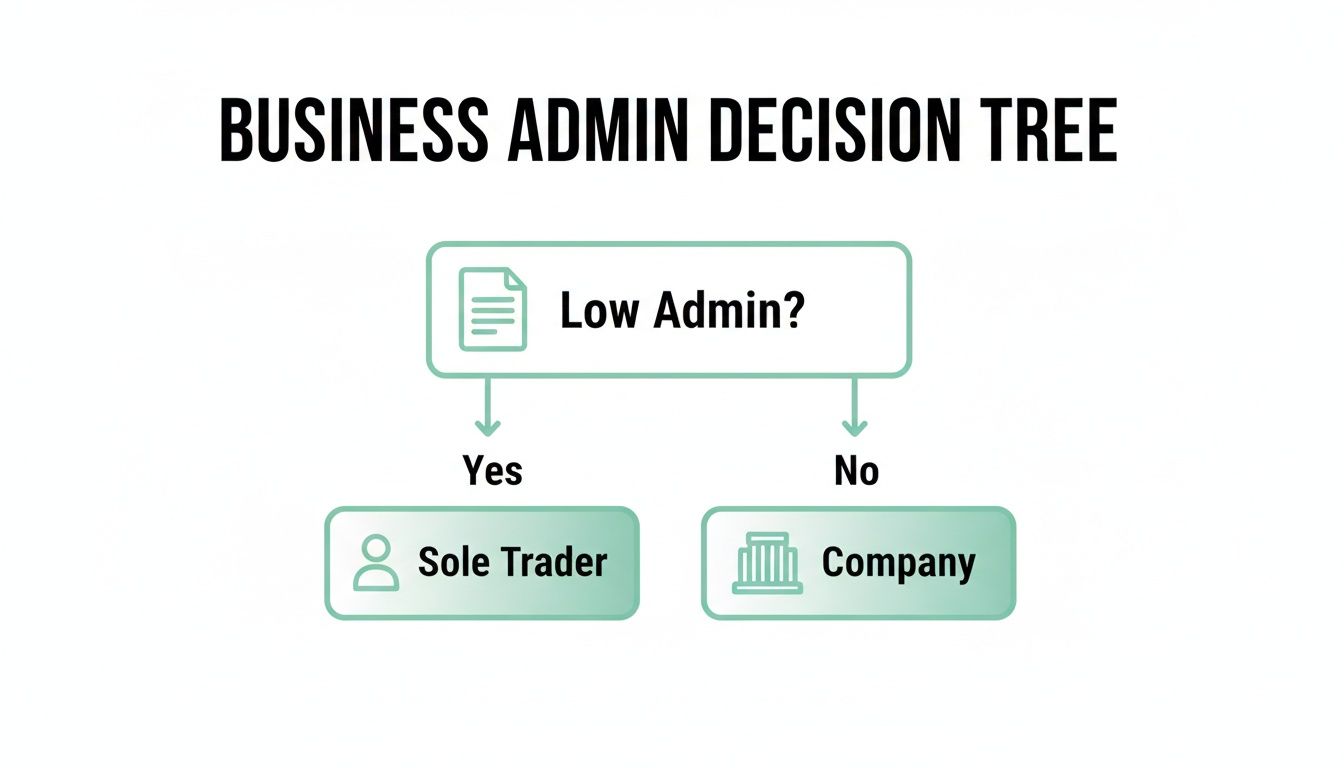

This decision tree boils it down to a simple question about your tolerance for admin.

As you can see, if keeping things simple is your top priority, the sole trader path is the clear winner. But if you’re prepared for more formal requirements, a company structure opens up a world of new possibilities.

Certain moments in your business's life are natural pivot points. They’re the little nudges telling you that what worked yesterday might not be the best fit for tomorrow. Let's walk through the big ones.

Your Income Is Climbing Steadily: As a sole trader, your business profit is just your personal income, taxed at your marginal rate. Once you start earning enough to push into the higher tax brackets (33% and 39%), the flat 28% corporate tax rate for a company starts looking very attractive. This is often the biggest financial trigger, and an accountant can quickly run the numbers for you.

You're Ready to Hire Your First Employee: The moment you bring someone onto the payroll, your responsibilities multiply. You’re now dealing with PAYE, employment contracts, and health and safety obligations. While you can hire staff as a sole trader, forming a company creates a much more professional and legally robust structure for being an employer. It cleanly separates those business obligations from your personal life.

You’re Taking on Bigger, Riskier Projects: Remember that unlimited personal liability we talked about? If you’re a freelance copywriter, the risk is pretty low. But if you’re a builder about to sign a contract for a major renovation, the potential for things to go wrong is significant. As the stakes get higher, the protection of a limited liability company becomes invaluable.

You Need to Seek Investment or a Loan: Banks and investors almost always prefer dealing with companies. A formal company structure looks more permanent, credible, and transparent. It gives them the confidence that you’re serious and that their money is going into a legitimate, well-documented entity. Trying to raise capital as a sole trader is an uphill battle, to say the least.

Switching isn't always the right move. Sometimes, sticking with the sole trader model is the smartest, most efficient choice you can make. What if you're not planning world domination?

Maybe you're a part-time consultant, a creative freelancer, or running a small side hustle alongside your main job. In these cases, the sheer simplicity of being a sole trader is a massive advantage. Why complicate your life with company admin and higher accounting fees if you don’t actually need the extra protection or tax benefits?

If your business is profitable, your risk is low, and you value simplicity above all else, staying a sole trader is a perfectly sound business decision. Don’t feel pressured to change just because it seems like the "next step."

Thinking about how to manage your time and output better is a core part of this decision. If you are leaning towards sticking as a sole trader, you might find some useful ideas in our article on how to improve business productivity. The right structure is simply the one that supports your goals, whatever they may be.

We’ve waded through a lot of the technical differences between being a sole trader and setting up a company. But let's be honest, theory is one thing, and the real world is another. There are always a few nagging questions that pop up when you're at this crossroads.

Let's jump into some of the most common ones we hear from Kiwi business owners.

Yes, absolutely. In fact, this is a well-trodden path for many successful New Zealand businesses and a natural part of the growth cycle.

The switch involves registering a new company with the Companies Office and getting a new IRD number for it. You'll then need to shift your sole trader assets and operations across to the new company. This means giving your clients a heads-up, opening new bank accounts, and updating your contracts.

It's a really smart move to get your accountant involved here. They can help with the tricky bits like valuing your assets for the transfer and making sure your final sole trader tax returns are filed correctly, saving you a world of pain down the line.

Generally speaking, companies find it easier to secure funding. Why? Because a company just looks more formal and permanent to lenders. It's a separate legal entity with strict reporting rules, which gives banks a clearer view of the finances and more confidence in the business.

That said, don't be surprised if the bank still asks for a personal guarantee from you as the director. This brings your personal assets back into the picture for that specific loan, but the formal company structure itself is still what they prefer to see. A sole trader can certainly get a loan, but the decision will be based entirely on their personal credit history and finances.

While not a legal requirement, opening a separate bank account as a sole trader is one of the best habits you can start with. Mixing business and personal spending is a recipe for an accounting nightmare come tax time.

This is a huge one, and the difference is pretty stark.

For a sole trader, the ongoing costs are minimal. Your main recurring expense will likely be your accountant's fee to prepare and file your annual IR3 tax return. It’s the leanest option by a country mile.

A company, on the other hand, comes with more built-in costs:

While being a sole trader is definitely cheaper day-to-day, the extra costs of a company are often a small price to pay for the liability protection and tax flexibility it offers a growing business. It’s a classic trade-off.

Feeling clearer, but still need help translating your business idea into a real-world digital product? The team at NZ Apps specialises in turning concepts into reality. Whether you need a custom web application or a sleek mobile app, we offer free consultations to help you find the right technology path. Find out how we can help your business grow.